When to Raise a Series A

by Aaron Harris5/22/2018

One of the hardest questions to answer when considering an A is “when is my company ready?” This is another one of those questions for which there are hundreds of answers on the internet, none of which are particularly satisfying. The reason these answers don’t work is that each rule has so many exceptions as to make the rule seem silly.

Founders often want clean and concrete answers as to when they’re ready to raise. This is why the idea that VCs filter exclusively on metrics is attractive. For instance: Saas companies are ready for an A when they cross $1m in ARR. This sounds good, but we’ve seen As happen for Saas companies with ARR between $200k and $9m with plenty of companies failing all along that range. Clearly VCs don’t care that much about this rule.

The other end of this set of advice says “raise when you can.” This is correct, but tautological. You only know that you can raise if you actually do so. It doesn’t form a coherent framework for deciding when to raise money.

I’ve been returning to this problem nearly every day since we started the Series A program and I’ve started to build a framework for how to solve it. Full disclosure – I don’t think there’s a perfect answer here, but I think having more context around why that answer doesn’t exist is helpful.

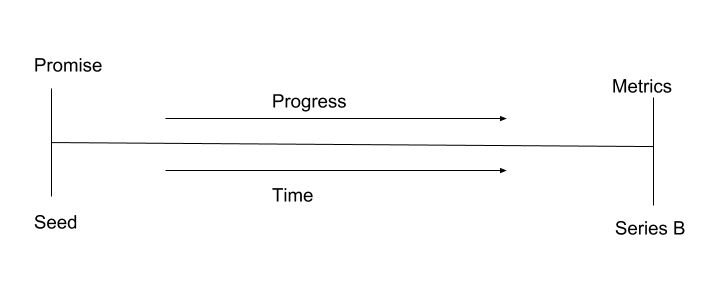

To understand what’s going on at the A round, it’s helpful to think of the decision process for funding as sitting along a horizontal axis. This axis roughly corresponds to the progression of a company from an idea to a functioning, scaling business. The decision process and the progress of the company are so closely related because – at each point in the life of a company – an investor looking at the company has the evidence of everything that the company has achieved up to that point. That evidence strongly informs that investor’s decision. The biggest gap in this axis is between Promise and Metrics, which maps to the seed round, and the B round.

Most seed rounds get raised based on the quality of the founders and the raw story that they can tell about their company and the future that company will create. By the Series B, those founders need to have accomplished a significant set of things that prove their ability to accomplish that future. This usually takes a few years, and comes with a set of in depth metrics about the health of the business and the impact of additional capital on that business.

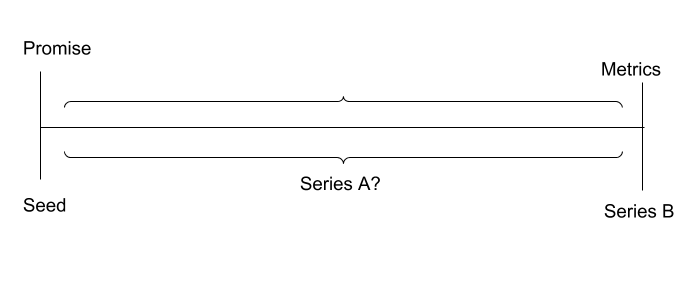

The reason the A is so hard to figure out is that it sits somewhere between these two points, and the point at which it sits differs based on the founders, the progress created, and the amount of time that the company has existed.

If you think of the A as being either a giant seed or a small B, then the conflicting advice starts to make sense because it’s all actually right and wrong depending on the specific situation. There are founders who can raise what looks like an A in dollar terms because they are so compelling. This will only work early on in the life of the company and before it has raised significant seed capital since time + money has to equal progress or investors will get suspicious.1

The longer a company has been in business – or the less good a founder is at telling a story – the more concrete and certain the metrics of that business need to be. Part of the challenge companies that have raised too much seed money face is that the requirements they face for an A are significantly higher than for those who raise less. They generally wait longer for their As, so investors expect to see associated progress.

As I said at the start, this doesn’t provide the sort of certainty I know founders want in answering the question of when to raise. However, I think that knowing that there is no clean answer is important because it provides a framework for thinking through the relative advantages you have when thinking about a raise.

One advantage of running a proper process when fundraising is that the early parts of the process are designed to let you test your story over time to see if it resonates. If it does, then you know you’re ready to raise an A. If not, keep working on the company until you are.

Notes

1. Though, as with all rules here, there are situations in which this rule gets violated by either a pivot or a founder who is just that good at telling stories.↩

Thanks to Craig Cannon for help writing this and to Marc Andreessen for helping me think it through.

Other Posts

Author

Aaron Harris

Aaron was a Group Partner at YC and a cofounder of Tutorspree, which was funded by YC in 2011. Before Tutorspree he worked at Bridgewater Associates, where he managed product and operations.